Credit is a vital aspect of our financial lives, affecting everything from our ability to buy a home to the interest rates we pay on loans. While many people understand the basics of credit scores, there’s a lot more to it than just a three-digit number. In this comprehensive guide, we’ll delve into the intricacies of credit and how it impacts your financial wellness.

Why Credit Education Matters

National Credit Education Month isn’t just a timely observance; it’s a reminder of the pervasive impact credit has on our lives year-round. Millions of Americans grapple with poor credit or lack of credit history, often unaware of how their financial behaviors influence their credit scores. Educating yourself about credit can empower you to make informed decisions and pave the way for a brighter financial future.

The Fundamentals of Credit

Understanding the fundamentals of credit is essential for managing your finances and achieving your financial goals. Credit plays a pivotal role in your ability to borrow money, secure loans, and access various financial products, making it crucial to grasp its key components and implications.

What is a Credit Score?

A credit score is a representation of your creditworthiness, ranging from 300 to 850. While a score above 700 is generally considered “good,” achieving a score above 750 or 800 can open doors to lower interest rates and better financial opportunities.

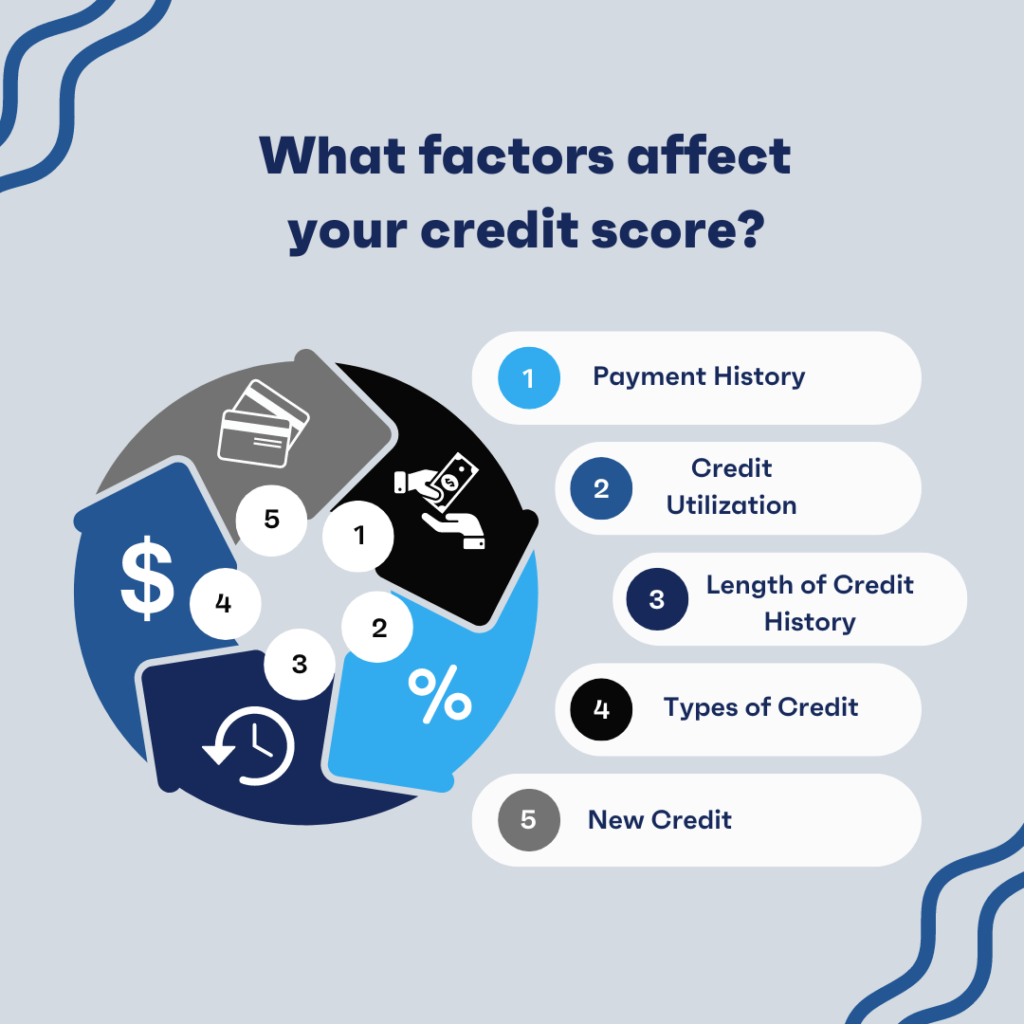

Factors Affecting Your Credit Score

Your credit score is influenced by various factors, including:

- Payment History: Consistently making on-time payments boosts your score.

- Credit Utilization: Keeping your credit card balances low relative to your credit limits is beneficial.

- Length of Credit History: Longer credit histories tend to result in higher scores.

- Types of Credit: Having a mix of credit accounts, such as credit cards and loans, can positively impact your score.

- New Credit: Opening multiple new credit accounts in a short period can lower your score.

Understanding these factors can help you take proactive steps to improve your credit score.

Building and Maintaining Good Credit

While it’s essential to have some debt to build credit and demonstrate your ability to manage borrowed funds responsibly, accumulating unnecessary debt can lead to financial stress and long-term challenges. Instead of viewing debt as a means to achieve immediate gratification, focus on responsible borrowing and timely repayments to maintain a healthy credit profile and financial stability. Here are a few suggestions to assist you in handling your credit efficiently:

Choose the Right Credit Card for Your Needs

Opening multiple credit cards can be beneficial for maximizing rewards and aligning with specific financial goals, such as earning travel points or cash back. However, it’s crucial to manage them responsibly to avoid negatively impacting your credit score. Applying for several cards in a short period can lower your average account age and may raise concerns for lenders. When deciding on the number of credit cards to have, consider your spending habits, ability to manage multiple accounts, and the benefits each card offers.

Determine whether you prefer cash back, travel rewards, or points that can be redeemed for various goods and services. Pay close attention to the card’s annual fees, interest rates, and additional features like purchase protection, extended warranty coverage, and travel insurance. Additionally, check if the card offers a welcome bonus, introductory 0% APR periods, or other promotional offers that can provide added value. Research different card offerings, compare their terms and benefits, and choose a card that aligns with your needs, financial situation, and long-term goals.

Use Your Credit Card Responsibly

Using credit cards responsibly is essential for maintaining a healthy financial profile. Timely payments are crucial for demonstrating financial responsibility, contributing to a positive payment history, and reducing negative marks on your credit report. Consistently paying your bills on time not only improves your creditworthiness but also lowers your credit utilization ratio and builds trust with lenders, paving the way for better loan terms and interest rates. To ensure you make timely payments, consider setting up automatic payments, creating payment reminders, and regularly monitoring your accounts.

While it may be tempting to max out a credit card, whether to cover monthly expenses or enjoy a vacation, doing so can have detrimental effects on your credit score and overall financial health. Maxing out your card may signal to lenders that you are overextended and at a higher risk of defaulting on payments.

If you find that your credit limit is too low, perhaps because you have been using a starter card or another low-limit card, consider updating your bank about your monthly income or requesting a credit line increase. This will help keep your utilization rate low and provide you with more financial flexibility. Remember, credit card debt can be challenging to manage, and it’s important to strive to pay off your balance every month to avoid the high interest rates often associated with credit cards.

Monitor Your Credit Report

Regularly check your credit report for errors and unauthorized accounts. You can check your own credit report as often as you’d like without it affecting your credit score. These are known as “soft inquiries” or “soft pulls.” Soft inquiries occur when you check your own credit report, and they do not impact your credit score.

On the other hand, “hard inquiries” or “hard pulls” occur when a lender or creditor checks your credit report as part of a credit application process. Hard inquiries can have a minor impact on your credit score and typically remain on your credit report for about two years.

It’s recommended to regularly check your credit report at least once a year from each of the three major credit bureaus (Equifax, Experian, and TransUnion) to monitor for any errors or fraudulent activity. You can obtain free annual credit reports from AnnualCreditReport.com, the only authorized source for free credit reports under federal law.

Take Advantage of Security and Fraud Protection

Credit cards often come with advanced security features and protections that offer greater peace of mind when making purchases. These may include fraud monitoring, zero liability protection, and secure encryption to safeguard your personal and financial information. Take advantage of these security measures by monitoring your account activity regularly, setting up transaction alerts for suspicious activity, and promptly reporting any unauthorized charges or potential signs of identity theft to your card issuer.

Many credit card issuers also offer additional layers of security, such as virtual card numbers for online shopping and biometric authentication methods like fingerprint or facial recognition for added protection. By prioritizing credit card security and maintaining vigilance over your credit card accounts, you can minimize the risk of identity theft, fraud, and unauthorized transactions, protecting both your credit and financial well-being.

Takeaways

Continuing to educate yourself about improving your credit is a continuous journey, not a one-time event. By understanding the nuances of credit and adopting responsible financial habits, you can build and maintain a strong credit profile that serves you well throughout your life. The overall goal is to leverage the benefits of credit cards while mitigating risks.

Remember, credit cards are financial tools that should complement your overall financial strategy, but if used improperly, they become financial pitfalls that can trap you in debt. With careful planning, smart decision-making, and ongoing education, you can maximize the benefits of credit cards, build a strong credit history, and achieve greater financial freedom.

For more insights on credit education or to explore financial wellness programs for your organization, contact the experts at Mentoro.